How to Register Dependents to Get Exemptions from Resident Tax

Resident tax (住民税) is a mandatory tax for individuals with income in Japan. However, you can reduce or even eliminate your resident tax by appropriately registering your dependents, helping you save more effectively. Let’s explore how with HSB JAPAN in this article.

Table of Contents

- What is Resident Tax?

- How Many Dependents Do You Need to Register to Reduce Resident Tax to Zero?

- Step 1: Determine Your Taxable Income

- Step 2: Identify the Resident Tax Exemption Threshold

- Step 3: Compare and Adjust to Bring Resident Tax to Zero

1. What is Resident Tax?

Resident tax (住民税) is a type of tax applied to the income of both citizens and foreign residents living in Japan. Its purpose is to ensure funding for local governments. The collected tax is used for education, welfare, waste management, disaster prevention, and cultural activities within the local community.

Anyone earning an annual income of 1,000,000 yen (100 man) or more is required to pay resident tax.

To be exempt from resident tax (i.e., bring it to zero), you typically need to adjust your taxable income (給与所得 – きゅうよしょとく) to be below the non-taxable threshold (非課税限度額 – ひかぜいげんどがく) set by your city or municipality.

2. How Many Dependents Do You Need to Register to Reduce Resident Tax to Zero?

Step 1: Determine Your Taxable Income

First, calculate your taxable income:

Taxable Income = Total Annual Income – Deductions (insurance, dependents, etc.)

You can calculate your taxable income based on your total annual income (給与年収) using the formula provided by your local tax office. Input your income into an online calculator (provided by the Tax Bureau) to get an estimate. Link

Step 2: Identify the Resident Tax Exemption Threshold

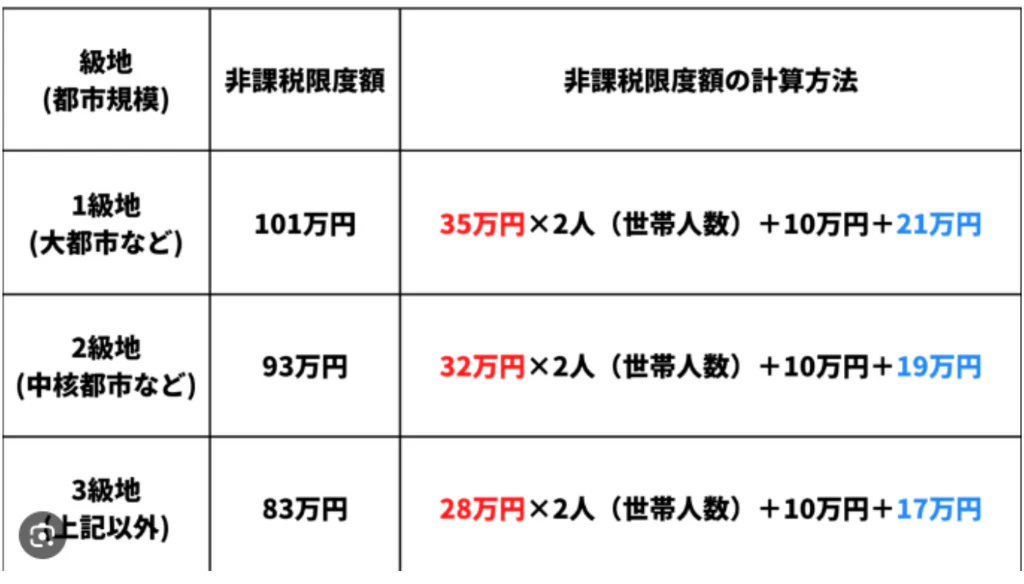

The exemption threshold varies depending on the number of dependents you register and the city you live in. Check whether your location falls under Area 1, 2, or 3 for specific thresholds.

For example, in Tokyo (Area 1), if your taxable income is less than:

- (35man×family members)+10man+21man(35 \text{man} \times \text{family members}) + 10 \text{man} + 21 \text{man}(35man×family members)+10man+21man,

then your resident tax will be zero.

Family Members (世帯人数) include:

- The household head,

- Dependent spouse (income below a certain threshold),

- Registered dependents (including dependents in Vietnam or Japan, as well as children under 16).

Step 3: Compare and Adjust to Bring Resident Tax to Zero

To eliminate resident tax:

Taxable Income < Resident Tax Exemption Threshold

For example:

- Total Annual Income: 3,000,000 yen (300 man) → Taxable Income: 2,020,000 yen (202 man).

- With 2 dependents: Exemption threshold = 1,360,000 yen (136 man) → Still taxable (202 man > 136 man).

- With 3 dependents: Exemption threshold = 1,710,000 yen (171 man) → Still taxable (202 man > 171 man).

- With 4 dependents: Exemption threshold = 2,060,000 yen (206 man) → Tax reduced to zero yen (202 man < 206 man).

If your income increases by around 300,000 yen (30 man) annually, you would only need to add one more dependent to maintain your resident tax exemption.

Conclusion

We hope this article is helpful for those seeking ways to reduce their resident tax! By understanding your income and registering dependents effectively, you can minimize your tax burden and save more for your needs.

Follow HSB JAPAN for more tips on managing taxes and documentation in Japan.